Flooding From Upstairs Apartments Closes Main Street Businesses. WhatInsurance Covers That?

/

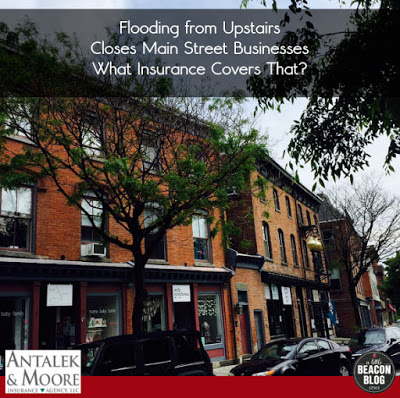

In the last two years, a few of your favorite businesses on Main Street have temporarily closed due to damage caused from flooding from residential apartments above them. Mountain Tops was one when their inventory got wiped out last summer, and Style Storehouse (pictured here) was almost another, but fortunately the owner Michele was in the store that day and could move her racks of clothing as the drips came from the ceiling.

Accidents happen, bath tubs are left on, sinks are left on, or maybe a pipe bursts. If this happens in your home, water that floods from your bathroom by leaving the shower curtain out of the tub, or by very wet children getting out of a full bathtub, may drip into the room below and possibly ruin nothing (or your floors), and perhaps only cause an inconvenient cleanup. But watch out for that invariably soggy ceiling that will need replaced. For a business located below a residential apartment, water can damage inventory, kitchen equipment, flooring that the business owner installed, and more financially devastating examples. When this happens, who pays for the damage? Who is responsible?

Pat Moore, partner at the local insurance agency on Main Street in Beacon,

, provides insight: "Water damage insurance claims can be very expensive, but can also be in a 'gray area' of insurance coverage. Even the most comprehensive of insurance policies do not eliminate the coverage 'gray area'."

What is the gray area? In Pat's words: "One requirement of all insurance coverages is that the damage needs to be caused by something that is sudden and accidental. For example, a deep freeze in the winter causes pipes to freeze and ultimately burst causing water damage. The act of freezing is generally considered to be sudden and accidental and most comprehensive insurance policies the business owner has will cover these damages."

So what about an apartment dweller who starts to fill the bathtub with water, gets distracted or forgets? The water overflows and now the business owner on the first floor has a small lake in their place of business. Says Pat: "This is certainly a gray area. Some insurance carriers may just decline to cover these kinds of incidents due to the lack of a sudden and accidental event. Others may decide to cover the damage with the hopes of making a recovery from the apartment dweller. If the apartment dweller has no homeowners insurance, this is not an attractive option to an insurance carrier. Some carriers may just cover the claim outright. How an insurance company will react is unpredictable."

Pat and the entire staff at

Antalek and Moore work with a number of insurance carriers

to find their clients the best coverage for competitive prices, and they have seen it all. Says Pat, as he recalls examples that have defined his years of experience in the insurance business: "It is important to understand what happened in this case. Unfortunately, the business owner sustained damage because the apartment owner was negligent. The relevant insurance policy for this case is the liability part of the apartment owner’s homeowners insurance."

When and if you ever lived in an apartment, did you carry

or

? Chances are low that you did because no one required you to, as you are required by a mortgage company to carry homeowner's insurance when you own a home financed through a bank.

Which brings Pat to an issue he is passionate about: "When a business owner seeks to occupy a commercial space, most landlords require the business to secure a

and to provide the landlord with written proof that insurance is in place. This is a common practice. A less common practice is the landlord making the same requirement of apartment dwellers. The cost for this coverage for an apartment dweller is typically $150 per year or less. Having an apartment dweller on the floors above who has an insurance policy in force should be a must have for any street level business.

"What does this do? In the case of the overflowing bathtub, the business can make a claim against the apartment dweller and his or her insurance policy. It mitigates the gray area." Also, a landlord might file a claim for the damage, and that may or may not be paid out by the insurance company. Further, says Pat, "The claim could be denied by the landlord's insurance carrier and will almost certainly not cover the damage to the business owner's property."

Consider this flipped way of thinking before you sign the lease on your commercial space. Chicken Little ran around warning his friends that the sky was falling, and while your inventory is inside and locked behind freshly installed locks and protected by a security system, the sky - and a lot of ceiling plaster - just may fall on and ruin all that is important to you and pays the bills for your family. If you are a person renting from an apartment above a business, consider getting

or several reasons, accidents like this being one of them.

is a sponsor of A Little Beacon Blog, and this article was created with them as part of our

program. It is with the support of businesses like this, that A Little Beacon Blog can bring you coverage of local happenings and events. Thank you for supporting businesses who support us! If you would like to become a

, please

click here for more information

.